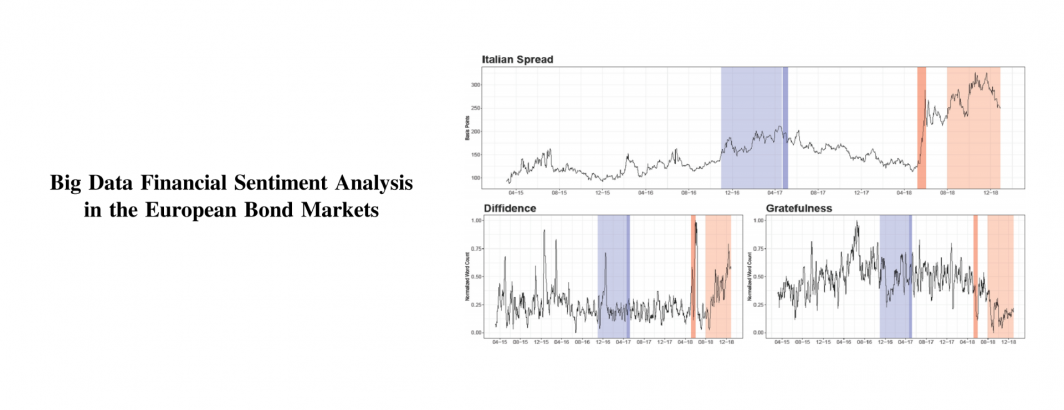

An interesting look at how the sentiment data in GDELT can be used to understand bond markets.

We exploit the novel Global Database of Events, Language and Tone (GDELT) to construct news-based financial sentiment measures capturing investor’s opinions for three European countries, Italy, Spain and France. We study whether deterioration in investor’s sentiment implies a rise in interest rates with respect to their German counterparts. Finally, we look at the link between agents’ sentiment and their portfolio exposure on the Italian, French and Spanish markets.