This fascinating paper by a group of researchers at the Joint Research Centre (JRC), Directorate A-Strategy, Work Programme and Resources, Scientific Development Unit, European Commission and the Department of Management of Universit'a Ca' Foscari Venezia explores economic forecasting using GDELT:

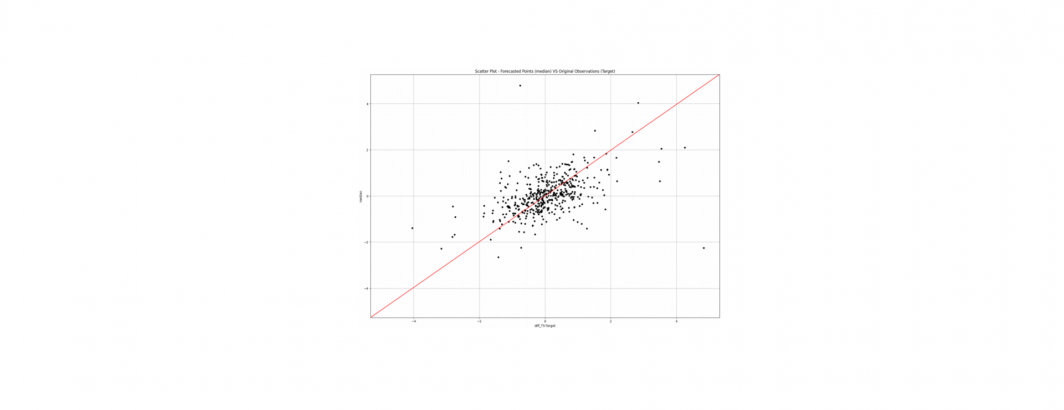

In this contribution we provide an overview of a currently on-going project related to the development of a methodology for building economic and financial indicators capturing investor’s emotions and topics popularity which are useful to analyse the sovereign bond markets of countries in the EU. These alternative indicators are obtained from the Global Data on Events, Location, and Tone (GDELT) database, which is a real-time, open-source, large-scale repository of global human society for open research which monitors worlds broadcast, print, and web news, creating a free open platform for computing on the entire world’s media. After providing an overview of the method under development, some preliminary findings related to the use case of Italy are also given. The use case reveals initial good performance of our methodology for the forecasting of the Italian sovereign bond market using the information extracted from GDELT and a deep Long Short-Term Memory Network opportunely trained and validated with a rolling window approach to best accounting for non-linearities in the data.