A new article by Sonja Tilly and Giacomo Livan uses news coverage to estimate market inflation expectations:

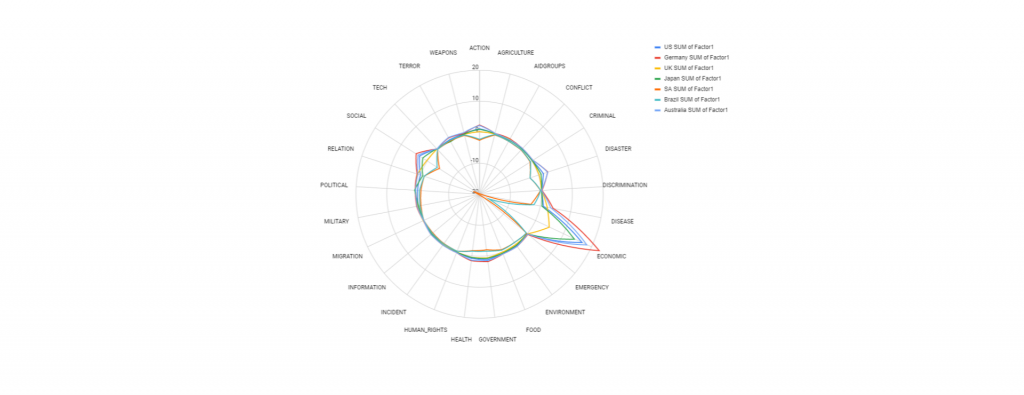

This study presents a novel approach to incorporating news topics and their associated sentiment into predictions of breakeven inflation rate (BEIR) movements for eight countries with mature bond markets. We calibrate five classes of machine learning models including narrative-based features for each country, and find that they generally outperform corresponding benchmarks that do not include such features. We find Logistic Regression and XGBoost classifiers to deliver the best performance across countries. We complement these results with a feature importance analysis, showing that economic and financial topics are the key performance drivers in our predictions, with additional contributions from topics related to health and government. We examine cross-country spillover effects of news narrative on BEIR via Graphical Granger Causality and confirm their existence for the US and Germany, while five other countries considered in our study are only influenced by local narrative.